Answer: When you purchase a life annuity and set your drawdown rate at, say, 5%, the product provider will calculate the drawdown at the start of the period, then divide it into 12 equal installments to give you the same pension each month.

If the markets fall during the year, your actual decline could be more than 5% in any given month.

A typical life annuity will cost around 3% per year and if you take 5% as income, your investment should return 8% per year so you don’t start to dip into your capital.

However, the first six months of this year have not been good for investors and stock markets have fallen by around 10%. If you picked the wrong investment portfolios, you could be in trouble.

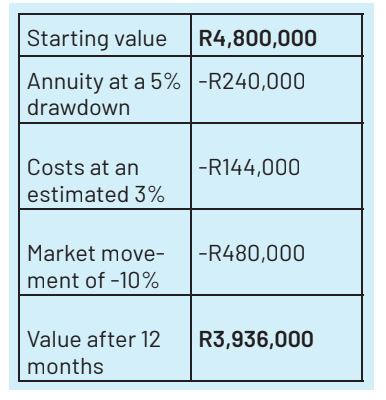

For example, if you purchased a R4.8 million life annuity with a 5% drawdown (which would earn you R20,000 each month) and the stock market fell 10% during the year , the lump sum in your life annuity would fall to just under R4 million after one year.

In order to maintain the same income of R20,000 per month, you will need to increase your drawdown percentage to 6.1%.

If you wanted to increase your monthly income by 6% to keep up with inflation, your withholding rate would need to increase to 6.5%. You move quickly into the area where you live off your capital rather than your investment income.

What can you do?

There are several things you can do to improve the situation:

Invest in portfolios with downside protection

Some portfolios use financial structures to limit any downward movement in the market. These include guaranteed funds, funds with high watermark guarantees, absolute return funds and real return funds.

There is an additional cost to these, but in the current circumstances they are worth considering.

Structure your life annuity portfolio carefully

I like to keep two years of income in a low-risk portfolio and take the monthly income out of it. This will save you from having to sell stocks when the market is doing badly. Keep the rest of your funds in longer-term growth assets.

Use part of your retirement savings to buy a life annuity

A recent change in the law allows you to buy both a life annuity and a life annuity with the proceeds of your retirement savings. Life annuity rates are good at the moment and by using part of your investment to purchase a life annuity, you can significantly reduce your life annuity drawdown rate. DM168

This story first appeared in our weekly newspaper Daily Maverick 168, which is available nationwide for R25.