[ad_1]

KUALA LUMPUR (September 29): The impact on the profits of insurers and takaful operators of premium deferrals as well as Covid-19 claims should remain manageable, with insurers and takaful operators assessed as resistant to stressed scenarios assuming claims higher than those observed so far, according to Bank Negara Malaysia (BNM).

Assumptions in stressed scenarios include ex gratia payments related to Covid-19 to policyholders and higher claims for policies without a pandemic clause, and a cautious increase in the ratio of general insurance claims to 17%.

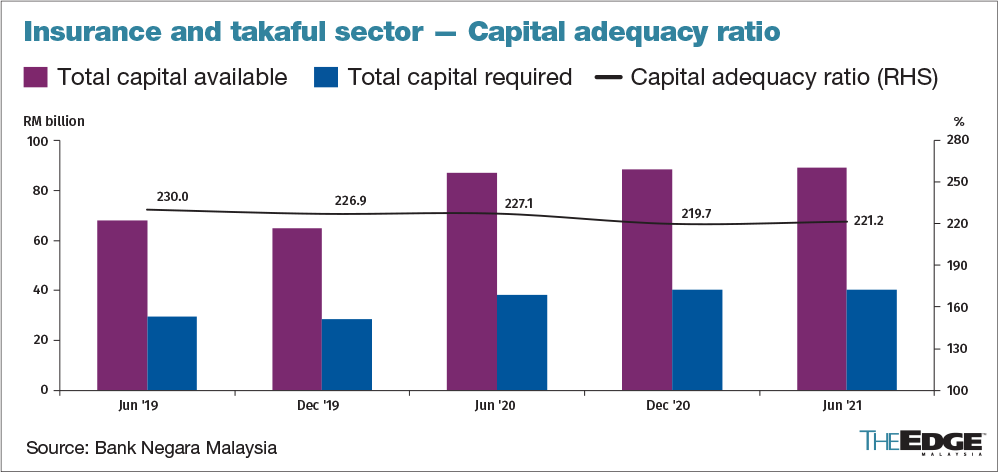

BNM noted that the industry’s overall capital adequacy ratio (ACR) of 221.2% remained well above the regulatory minimum of 130%. All insurers and takaful operators also continued to maintain capital ratios above their internal capital target levels which ranged from 150% to 250%.

At the end of June 2021, the aggregate excess capital buffers above the regulatory minimum stood at RM36.8 billion.

“Going forward, financial market volatility and the prospect of higher bond yields will continue to weigh on the earnings of insurers and takaful operators given their significant financial investments. Nevertheless, the insurance and takaful sector should remain resilient, â€said BNM in its Financial Stability Review report for the first half of 2021 (1H21) published on Wednesday.

“A sensitivity analysis carried out on the balance sheets of insurers and takaful operators showed a limited impact on their solvency positions in the event of a sharp rise in bond yields. This is supported by their strong capitalization, â€he added.

{kind=link}

The central bank noted that some life and family insurers and takaful operators have introduced additional underwriting measures, including questionnaires to assess the medical history of Covid-19 and risk exposure of potential policyholders, as they take into account the increased risks resulting from the pandemic.

It also observed that in certain cases, the insured persons concerned could be subject to additional subscription conditions, such as longer waiting periods. A higher premium charge could also be imposed on policyholders with indications of a higher risk of developing serious health problems, although this largely depends on additional medical assessments carried out on a case-by-case basis.

Nonetheless, the BNM said such practices had so far not been widely observed to suggest a broader tightening of underwriting terms between insurers and takaful operators due to Covid-19.

“The impact on life and family insurers and takaful operators of the temporary relief measures granted to policyholders has remained limited. Affected policyholders were able to defer premiums due under life insurance policies and family takaful certificates for three months without interruption of their coverage. This option, which was due to expire by June 2021, has been extended until December 2021. “

Policyholders who used the premium deferral option continued to increase, although the amount of premiums deferred and covered by premium holidays remained relatively low at 8.3% of premiums in effect between March 27, 2020. and September 3, 2021.

Premium leave refers to continued takaful insurance / coverage despite no premium payment and applies to products with the premium holiday feature already in place, such as investment related products.

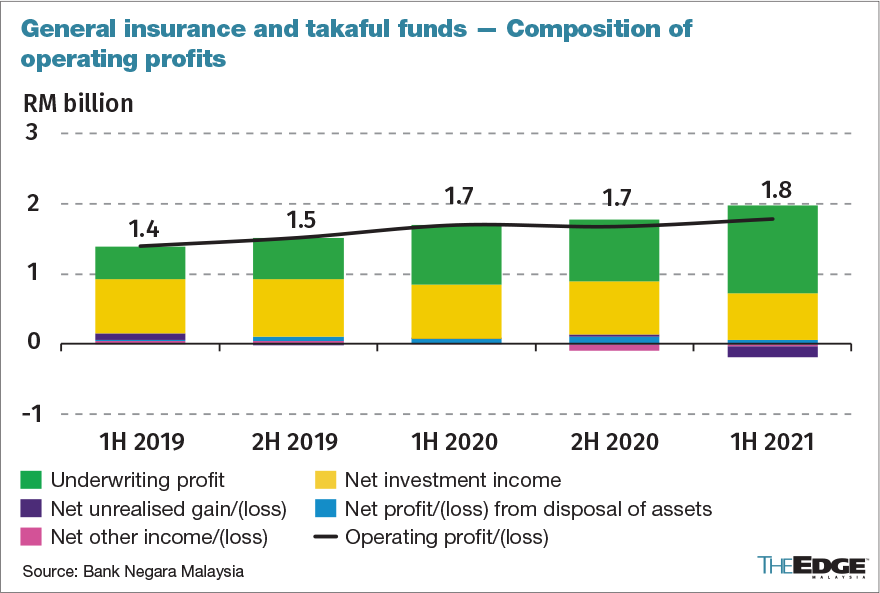

Profits for general and takaful insurers improve slightly in 1H

General insurance and takaful funds saw a slight increase in operating profit to RM 1.8 billion in 1H21 from RM 1.7 billion in 1H20, thanks to better underwriting performance.

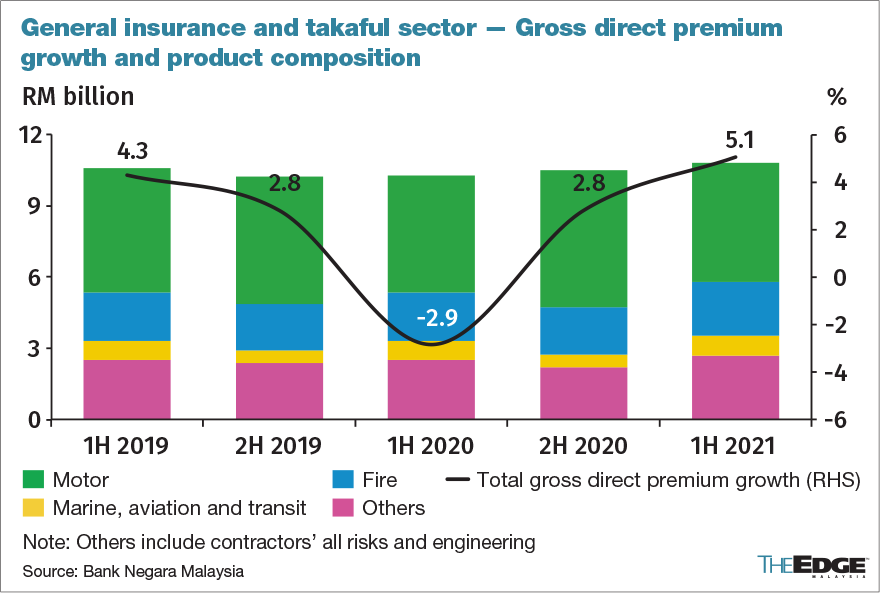

Gross direct premiums have been bolstered by revised premium rates for the fire, contractor, and engineering segments following higher claims resulting from several major fires and explosions over the past two years, according to BNM.

Higher premiums were also supported, to a lesser extent, by a recovery in the automotive segment amid rebounding car sales following the extension of the vehicle sales tax exemption, which is in place. until December 2021, and the relaxation of containment measures before the full movement control order (FMCO).

However, BNM noted that some small insurers and takaful operators continued to experience considerable profit volatility in 1H21 due to a greater reliance on investment income to support overall profitability.

“The risk of increased volatility in financial markets therefore remains significant for these insurers and takaful operators,” he said.

[ad_2]